Nothing ever happens

Why 72% of prediction market contracts resolve to NO; first analysed on 161,638 contracts across polymarket and kalshi, then extended to 1.77 million contracts on Kalshi.

The Pattern

I analyzed 161,638 prediction market contracts across Polymarket and Kalshi. The finding that kept showing up:

72% of contracts resolve NO.

Not 50%. Not 60%. Seventy-two percent.

At first, this seems to confirm every cynic’s favorite phrase: “Nothing ever happens.” Markets are biased. Prediction markets overestimate change. The status quo wins.

But that explanation is wrong.

The 72% isn’t a bug. It’s not bias. It’s math—and understanding why reveals something profound about how prediction markets actually work.

The Data

Before diving into explanations, here’s exactly what we found:

The pattern is consistent across both platforms. This isn’t a quirk of one exchange—it’s structural.

When we expanded our analysis to Kalshi’s full contract history (1.77 million contracts), the pattern held but revealed something more nuanced:

Three completely different patterns. Three completely different explanations.

The Naive Interpretation

Here’s what most people assume when they hear “72% resolve NO”:

“People are too optimistic. They overestimate the probability of events occurring. Markets are inefficient.”

This interpretation spawned a cottage industry of “NO maximalists” — traders who blindly short every YES position, assuming the crowd is systematically wrong.

Some even built strategies around it. “Just bet NO on everything. The base rate is on your side.”

The problem? This strategy doesn’t work.

The data shows NO bettors don’t systematically outperform YES bettors. If 72% NO was a true market inefficiency, NO traders would be printing money.

They’re not.

So what’s actually happening?

The Mathematical Reality

The 72% NO rate isn’t about market psychology. It’s about market structure.

In 1945, Friedrich Hayek argued that markets solve society’s “knowledge problem” by aggregating dispersed information through prices. But how markets are structured matters enormously for this aggregation to work effectively.

Different contract types have mathematically determined resolution patterns—and understanding these patterns is the key to understanding the 72%.

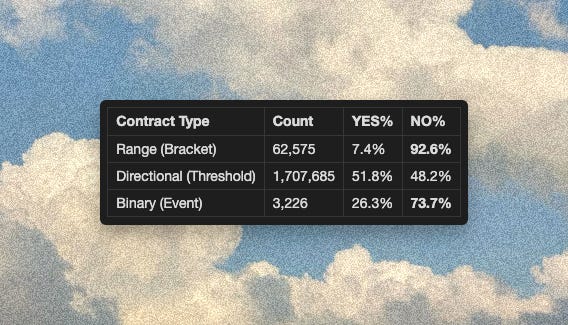

Range Contracts: 92.6% Resolve NO (By Design)

Consider a market like “Where will the S&P 500 close on January 19, 2024?”

Kalshi doesn’t ask this as a single question. Instead, it offers 15-25 range brackets covering the full distribution:

Event: "Where will S&P 500 close on Jan 19, 2024?"

The market offers 15 brackets covering the full range:

├── 4625-4649 → 6.7% implied probability

├── 4650-4674 → 6.7% implied probability

├── 4675-4699 → 6.7% implied probability

├── ... (12 more brackets)

└── 4925-4949 → 6.7% implied probability

Result: 14 brackets resolve NO, 1 resolves YESBy construction, 14 of 15 contracts MUST resolve NO. Only one range can contain the actual closing value.

This isn’t bias. It’s arithmetic.

When you create multi-outcome events with range structures, you’re mathematically guaranteeing a high NO resolution rate. If an event has 15 possible outcomes, 14/15 (93.3%) will resolve NO — regardless of whether markets are efficient or not.

Why this design matters:

Range contracts capture something binaries can’t: the full probability distribution.

Central tendency: Which range has the highest price? That’s the market’s best guess.

Dispersion: How spread out are the prices? That’s the market’s uncertainty.

Tail probabilities: What’s the 5% range trading at? That’s explicit black swan pricing.

You can’t get this from “Will S&P go up?” You need the granularity.

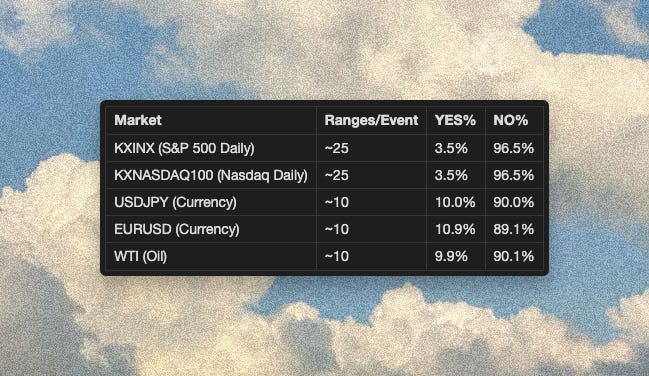

Here’s how resolution rates vary by specific range market:

More ranges = more precise probability distribution = lower per-contract YES rate.

Directional Contracts: ~50% Resolve NO (Market Efficiency)

Now consider a different structure: “Will the S&P 500 close above 4,500?”

This is a single threshold. Either it does or it doesn’t.

For these contracts, the resolution rate is almost exactly 50/50:

YES: 51.8%

NO: 48.2%

Why? Because efficient markets set thresholds at the expected value.

If the market thinks S&P will close at 4,500, and Kalshi sets the threshold at 4,500, then:

~50% of the time it closes above

~50% of the time it closes below

This is the Efficient Market Hypothesis in action. Not a design quirk, not bias—just markets doing what markets do.

When directional contracts show systematic deviation from 50/50, that’s when you should pay attention. It means either:

Thresholds are poorly set, or

There’s genuine directional information in the market

Binary Contracts: 73.7% Resolve NO (Reality)

True binary questions — “Will X happen?” with no structural relationship to other contracts — show a different pattern.

These resolve NO about 74% of the time.

This is the closest thing to genuine “nothing ever happens.”

Most discrete events don’t occur:

Mergers fall through

Legislation stalls

Announcements get delayed

The Fed holds rates

Candidates don’t drop out

The status quo has genuine inertia. Mean reversion is real.

But here’s the crucial insight: markets know this. A binary at 30% YES already incorporates status quo bias into the price. The 74% NO rate isn’t an exploitable inefficiency—it’s accurate pricing of reality.

Consider Fed decision markets on Kalshi:

The Composition Effect

Here’s where it all comes together.

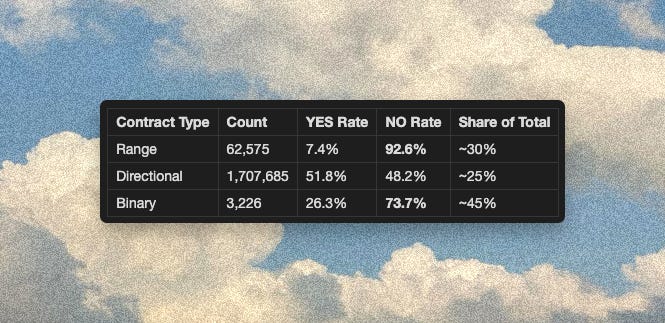

The aggregate 72% NO rate is a weighted average of three different phenomena:

The overall 72% emerges from mixing these different structures. It’s not a single phenomenon — it’s three different phenomena with three different explanations:

Range contracts (92.6% NO): Mathematical necessity

Directional contracts (48.2% NO): Market efficiency

Binary contracts (73.7% NO): Status quo inertia

Treating them as one thing leads to wrong conclusions.

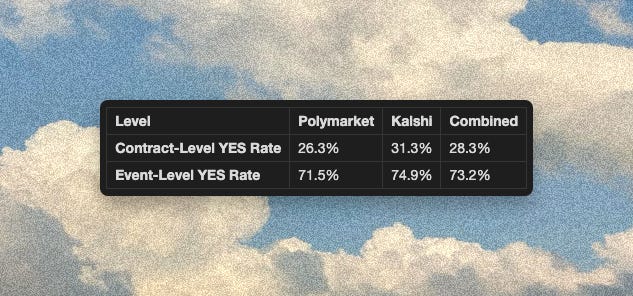

Event-Level vs Contract-Level: A Critical Distinction

There’s another layer of confusion in the “nothing ever happens” narrative: conflating contract-level and event-level resolution.

Wait—at the event level, YES wins 73% of the time?

Yes. Here’s why:

A single event like “The Open Championship” generates multiple contracts:

“Will Player A win?” → NO

“Will Player B win?” → NO

“Will Player C win?” → YES

... (20 more players) → NO

At the contract level, 22 of 23 resolve NO.

At the event level, ONE winner is guaranteed—so YES happens 100% of the time.

The event-level rate counts “at least one YES” per event. This is naturally higher because multi-contract events (tournaments, elections with many candidates) typically have exactly one winner.

The takeaway: Always specify whether you’re analyzing contracts or events. They tell different stories.

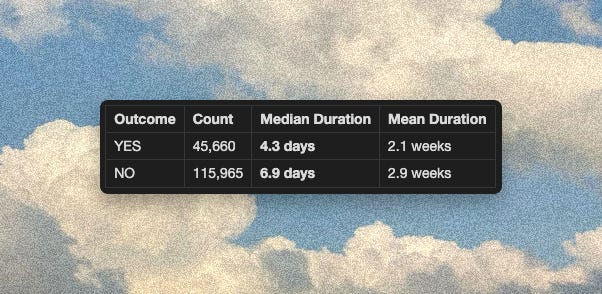

Time-to-Resolution: YES Contracts Resolve Faster

Our analysis revealed another pattern:

YES contracts resolve 2.6 days faster on median.

Why? Events that happen tend to happen quickly. Events that don’t happen wait for the scheduled end date.

Think about it:

“Will the CEO resign this quarter?” → If yes, it’s announced and resolved immediately

“Will the CEO resign this quarter?” → If no, you wait until the quarter ends

This has implications for traders. YES positions that are correct resolve faster, freeing up capital. NO positions tie up capital longer, even when correct.

Why This Matters for Traders

If you’re trading prediction markets, the 72% number is useless. What matters is understanding which type of contract you’re trading.

Trading Range Contracts

The 92.6% NO rate isn’t edge — it’s priced in. Markets know most ranges won’t hit.

A range trading at 5% isn’t a good short just because “ranges usually resolve NO.” The question is whether this specific range is mispriced relative to its true probability.

Your edge must come from better distribution estimation. Where will the outcome actually land? Is the market underpricing volatility? Are the tails too cheap?

Trading Directional Contracts

These are the closest to “fair” games. The ~50/50 split means there’s no structural edge from direction alone.

Your edge has to come from better probability estimation. Do you know something about the Fed’s likely decision that the market doesn’t? That’s edge.

Betting NO because “nothing ever happens” isn’t a strategy—it’s a meme.

Trading Binary Contracts

The 74% NO rate on binary events is the most interesting finding—but also the most misunderstood.

Here’s the catch: markets already incorporate status quo bias into prices. A binary event priced at 30% YES isn’t necessarily a good short just because “most binaries resolve NO.”

The question is whether 30% is the right price for this specific event.

If anything, our data suggests a slight favorite-longshot bias: longshots (low-probability events) actually win slightly more often than their prices imply. But the effect is small—not enough to overcome transaction costs for most traders.

Hayek Was Right (And This Proves It)

Step back and the 72% reveals something profound about prediction market architecture.

In 1945, Hayek argued that no central planner can aggregate the dispersed, local, dynamic knowledge held by millions of individuals. Markets solve this through prices.

Prediction markets go further—they don’t just aggregate knowledge about what to buy, they aggregate knowledge about what will happen.

Kalshi’s multi-contract architecture demonstrates how:

Range contracts capture the full probability distribution—not just “up or down” but “by how much”

Directional contracts enable continuous price discovery around expected values

Binary contracts aggregate beliefs on discrete outcomes

The “92% NO” in range contracts isn’t failure—it’s success. It’s the market saying “here’s the full distribution of possibilities, priced in real-time.”

Traditional exchanges (stocks, futures, options) trade continuous variables. Prices can be any value.

Prediction markets convert uncertain futures into discrete, tradeable contracts. This conversion process creates structure that influences resolution patterns.

A single event like “What will GDP growth be?” can become:

One binary contract (”Above 2%?”)

One directional contract (”Above/below 2.5%?”)

Multiple range contracts (”1-1.5%”, “1.5-2%”, “2-2.5%”, etc.)

Same underlying uncertainty. Completely different resolution statistics.

The 72% isn’t telling us about the world. It’s telling us about how we’ve chosen to slice up the world into tradeable pieces—and that slicing is what enables Hayek’s vision of decentralized knowledge aggregation.

Implications

For Traders

Stop using aggregate resolution rates as trading signals. Understand the contract structure you’re trading. The edge is in the specifics, not the averages.

For Researchers

When studying prediction market accuracy, control for contract type. Mixing ranges with binaries produces misleading calibration statistics.

For Market Designers

The choice of contract structure isn’t neutral. Range contracts create different incentive structures than binaries. The 72% NO rate is partly a design choice—and a good one for capturing full distributions.

Methodology

Data Sources:

Polymarket: Gamma API (

https://gamma-api.polymarket.com/markets)Kalshi: Native API + Dome API

Resolution Logic:

Polymarket: Winner inferred from

outcomePrices(price > 0.9 = winner)Kalshi: Explicit

resultfield

Contract Classification (Kalshi):

Range:

-Bsuffix in ticker (verified 100% accuracy via manual sampling)Directional:

-Tsuffix in ticker (verified 100% accuracy)Binary: Neither suffix

Sample Sizes:

Polymarket binary contracts: 98,522

Kalshi total contracts: 1,773,486 (including range and directional)

Time period: 2021-2025

Full code and replication instructions available at github.com/kluless13/pm-data-analyses

The Bottom Line

“Nothing ever happens” is a meme, not a trading strategy.

The 72% NO resolution rate comes from three different sources:

Mathematical necessity in range contracts (92.6% NO by design)

Market efficiency in directional contracts (50/50 as expected)

Genuine status quo inertia in binary events (74% NO reflects reality)

Understanding which one you’re trading is the difference between having an edge and having a narrative.

The data doesn’t lie. But it doesn’t interpret itself either.

And if you’re still tempted to “just bet NO on everything”—remember that the prices already incorporate everything you think you know about base rates.

The question isn’t “do most contracts resolve NO?”

The question is “does this specific contract resolve NO more often than its price implies?”

That’s a much harder question. And the answer is usually: probably not.

Based on analysis of 161,638 contracts across Polymarket and Kalshi, with extended analysis of 1.77 million Kalshi contracts. Full methodology documented for peer review.