The Dollar Does the Tightening

June 24, 2026 | Overnight Macro #0003

The Overnight Read

The overnight message was tighter financial conditions without a fresh policy move: tech cracked, the dollar held firm, long Treasuries stabilized, and oil backed off. The market is doing some of the Fed’s work before the next major U.S. inflation checkpoint. Source: https://www.wsj.com/finance/stocks/stocks-retreat-as-fears-deepen-about-strength-of-ai-boom-b0c9a310

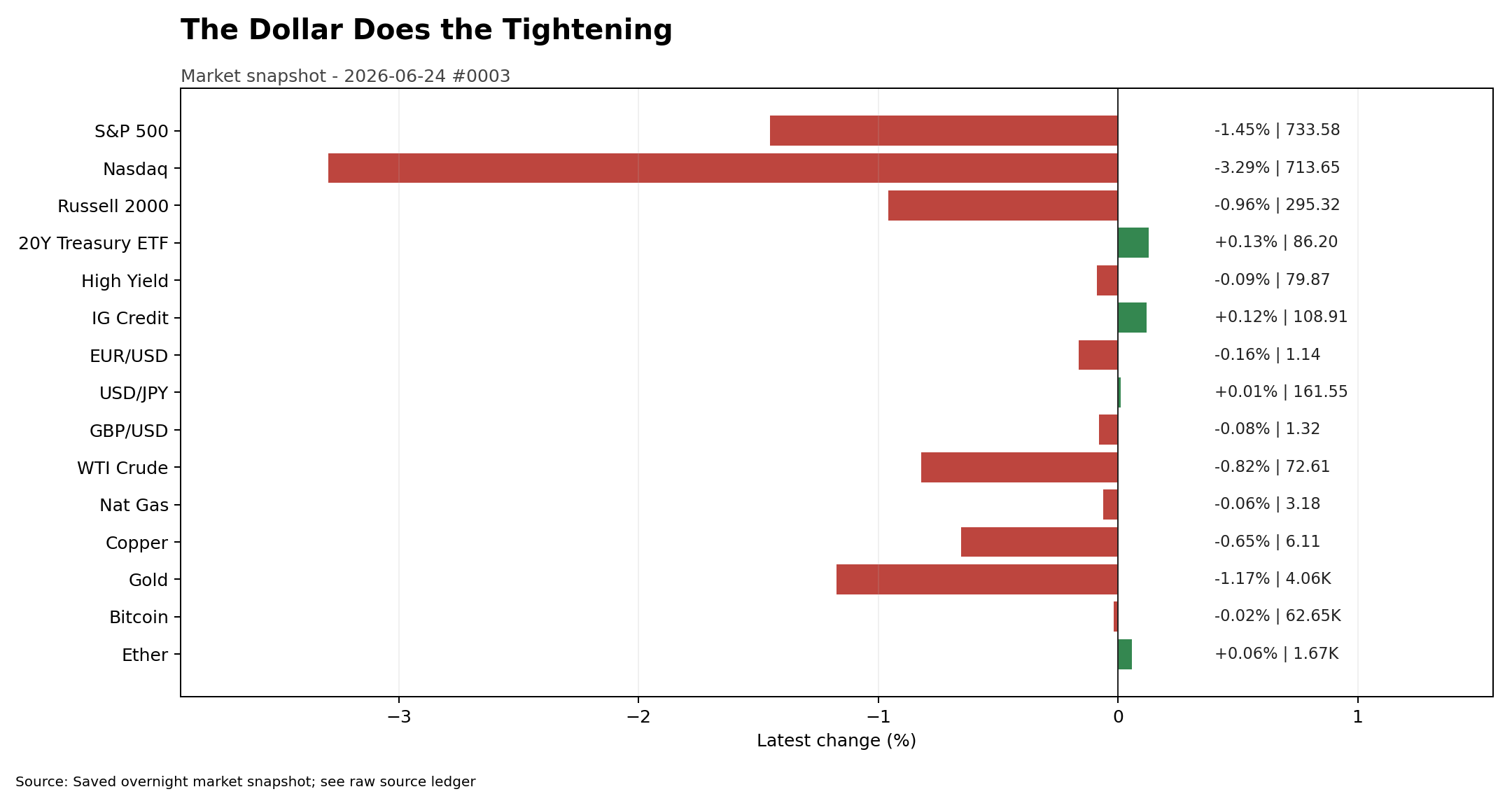

U.S. equities lost altitude through the growth-and-AI complex, with SPY down 1.45% and QQQ down 3.29%, while VIX jumped to 19.49. That rotation mattered more than the modest move in headline rates because it tightened risk appetite directly.

The dollar stayed in charge against both Europe and Japan. EUR/USD slipped to 1.1373 as euro-area data and ECB rhetoric stayed soft, while USD/JPY hovered near 161.6 with intervention risk still hanging over the tape.

The next real macro gate is the calendar, not the post-close noise. German confidence, Australian labor and inflation follow-through, U.S. PCE, and then China and euro-area inflation data will decide whether this becomes a short-lived tech wobble or a broader duration-and-dollar squeeze.

The Map

The cross-asset overnight setup

The forward macro calendar

Commodities and the inflation channel

Rates, curves, and central-bank pressure points

FX, especially the euro and yen

Equities, credit, crypto, and DeFi

Truflation real-time signals

Country-level macro context

Catalyst tape, Twitter discourse, and next watch points

Markets Tighten Before Policymakers

The cleanest way to frame the session is that markets tightened before policymakers did. The overnight market snapshot showed SPY at 733.58, down 1.45%, QQQ at 713.65, down 3.29%, and VIX at 19.49, up 12.79%. TLT added 0.13% while BTC and ETH were nearly unchanged, which is a classic sign that cross-asset stress was concentrated in crowded equity leadership rather than a system-wide liquidation.

The headline catalyst in public coverage was a harder reset in AI and semiconductor enthusiasm. Barron’s described a broad AI-led shakeout, and the Wall Street Journal framed the move as a deeper challenge to the durability of the boom rather than a one-off wobble. Sources: https://www.barrons.com/articles/stocks-today-ai-jitters-chip-selloff-3b969fc0; https://www.wsj.com/finance/stocks/stocks-retreat-as-fears-deepen-about-strength-of-ai-boom-b0c9a310

What mattered for macro, though, was the transmission channel. The growth scare pushed investors toward duration, helped pull oil off the boil, and left the dollar firm anyway. That combination is tighter for global liquidity even without a fresh move higher in nominal Treasury yields.

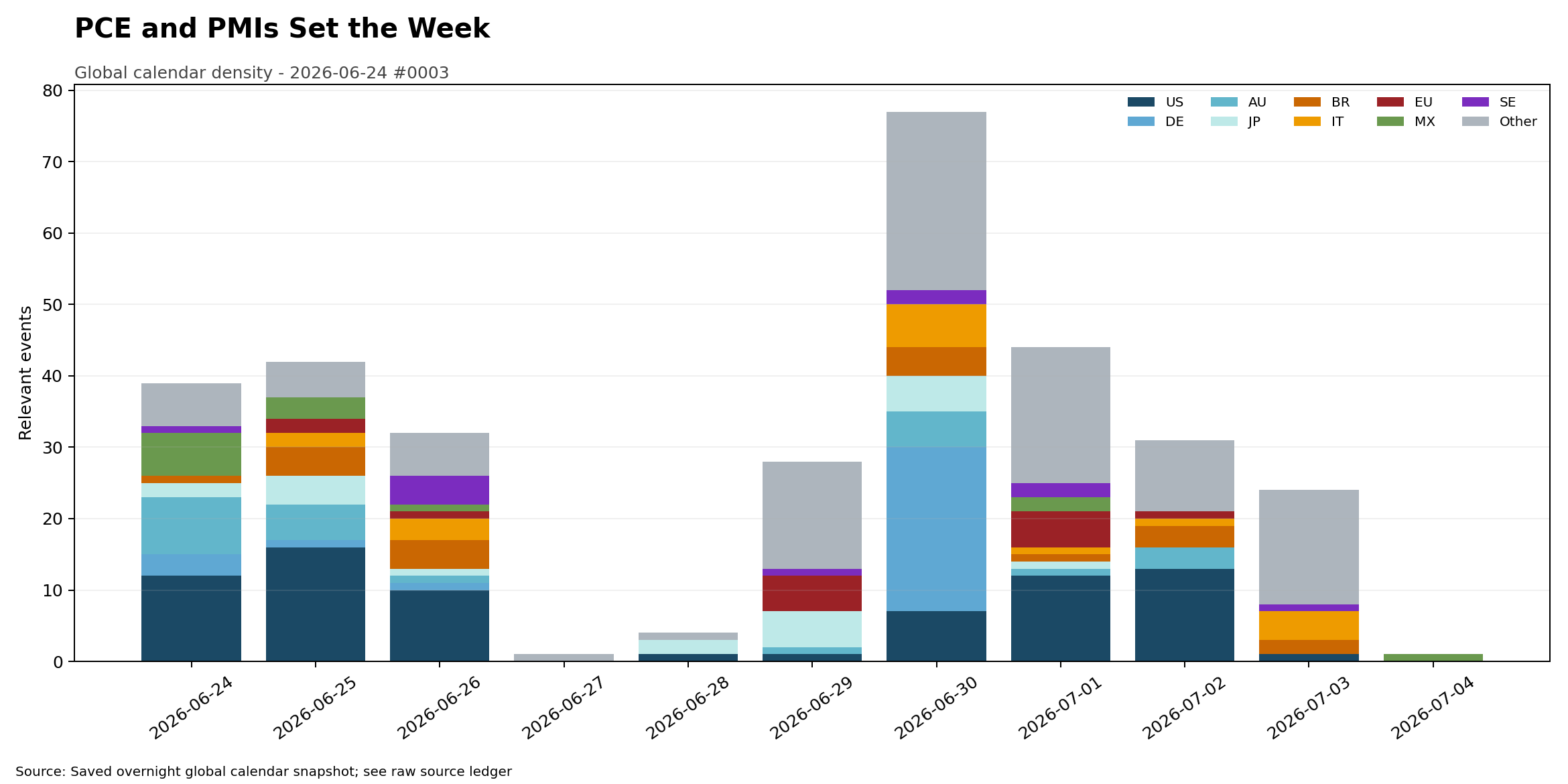

PCE and PMIs Set the Week

The next 24 to 48 hours are more important than the overnight tape itself. Germany’s June Ifo read and Australian inflation follow-through sit up front, while U.S. current account data and crude inventories fill in the near-term backdrop. After that, the desk focus turns squarely to U.S. May Core PCE, Personal Income, Personal Spending, and Durable Goods on Thursday, June 25, 2026.

Beyond the immediate window, the run into month-end is dense. China’s June PMIs land on Tuesday, June 30, 2026, followed by euro-area inflation prints and then U.S. ISM manufacturing and Friday payrolls in the next leg. If the market is already tightening through equities and FX, these are the releases that can either validate the move or reverse it fast.

Oil Slips, Gold Loses Cover

Crude looked less like a geopolitical squeeze and more like a growth-sensitive asset overnight. The market snapshot put crude at 72.48, down just under 1%, even as supply-security rhetoric stayed alive in Washington. That tells you demand expectations and broader risk reduction mattered more than immediate scarcity fears in this session.

Gold also lost some shelter. The overnight market snapshot showed XAU/USD at 4087.94, down 0.55%, which fits better with a stronger dollar and a recalibration of Fed expectations than with a pure safe-haven bid. Source: https://www.fxstreet.com/news/gold-loses-ground-to-near-4-100-as-inflation-concerns-fed-rate-hike-bets-build-202606232313

Copper softened only modestly, which matters because the metal did not fully confirm the severity of the equity move. That leaves the commodity message mixed: energy is easing, precious metals are yielding to the dollar, and industrial metals are not yet fully endorsing a hard landing call.

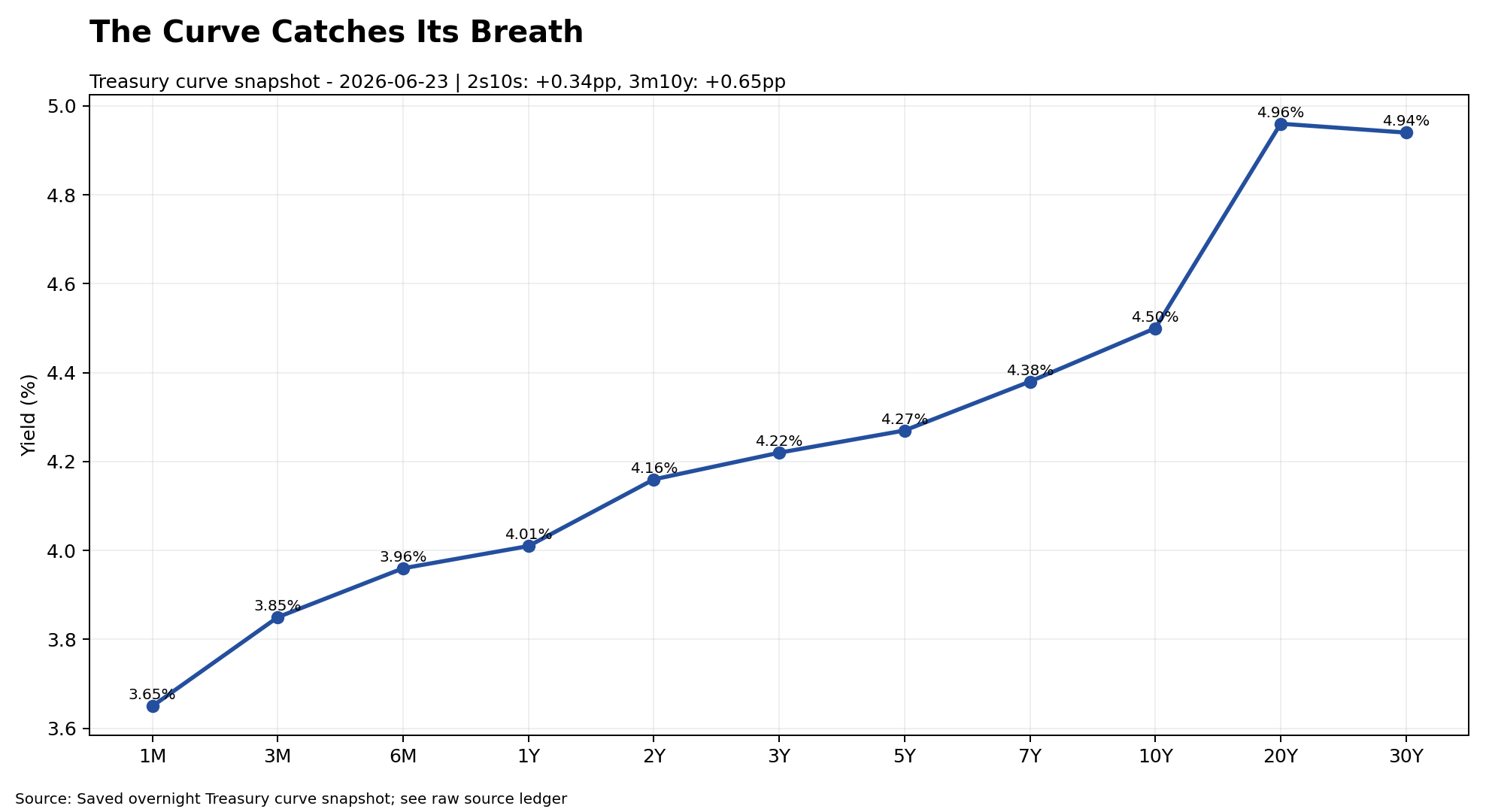

The Curve Catches Its Breath

Treasuries caught their breath rather than staging a full relief rally. The overnight Treasury curve had the 2-year at 4.16%, the 10-year at 4.50%, the 30-year at 4.94%, and the 2s10s spread at +34 basis points. The curve is no longer inverted in either 2s10s or 3m10y terms, which keeps the debate centered on re-steepening rather than recession signaling.

The important nuance is that rates did not need to collapse for financial conditions to tighten. Bloomberg’s market coverage on X pointed to a rise in Treasuries as stocks sold off and oil fell, trimming bets on future Fed hikes. That is consistent with the overnight curve: some relief on duration, but not enough to offset the broader dollar-and-equity tightening.

The calendar now matters more than the last basis point on the 10-year. Core PCE at 0.3% month on month versus 0.2% prior is the most obvious swing factor for the front end.

Dollar Firm, Yen Fragile

The dollar stayed firm where it mattered most. EUR/USD slipped to 1.1373 in the overnight market snapshot, and Bloomberg’s euro coverage on X tied the move to weak data and dovish ECB commentary. That keeps the macro burden on Europe: softer activity still coexists with an inflation debate that is not cleanly over.

USD/JPY at 161.58 remains the more dangerous FX signal. Reuters highlighted that the yen is hovering near a forty-year low, with dollar strength overwhelming Bank of Japan adjustments. Bloomberg also flagged weak demand at Japan’s five-year bond auction, reinforcing the sense that policy credibility and currency pressure are colliding.

In plain terms, the FX tape says the U.S. is exporting tighter conditions. Europe gets it through a weaker euro and soft data, while Japan gets it through a structurally fragile yen and intervention risk.

AI Mania Meets Gravity

Equities absorbed the real shock. The overnight market snapshot showed SPY down 1.45%, QQQ down 3.29%, XLK down 4.14%, and Industrials down 2.01%, while defensives like Consumer Staples and Health Care were positive. That is not broad panic, but it is a meaningful rotation out of expensive cyclicality and AI concentration.

Public coverage lined up with that read. Barron’s emphasized a broad tech and chip retreat, and the Wall Street Journal said fears around the durability of the AI boom were driving the selloff. Sources: https://www.barrons.com/articles/stocks-today-ai-jitters-chip-selloff-3b969fc0; https://www.wsj.com/finance/stocks/stocks-retreat-as-fears-deepen-about-strength-of-ai-boom-b0c9a310

Credit was more orderly than equities. HYG slipped only 0.09% while LQD rose 0.12% in the overnight market snapshot, suggesting this was still more of a valuation and leadership reset than a genuine funding scare.

Fear Runs Hot, Liquidity Stays Concentrated

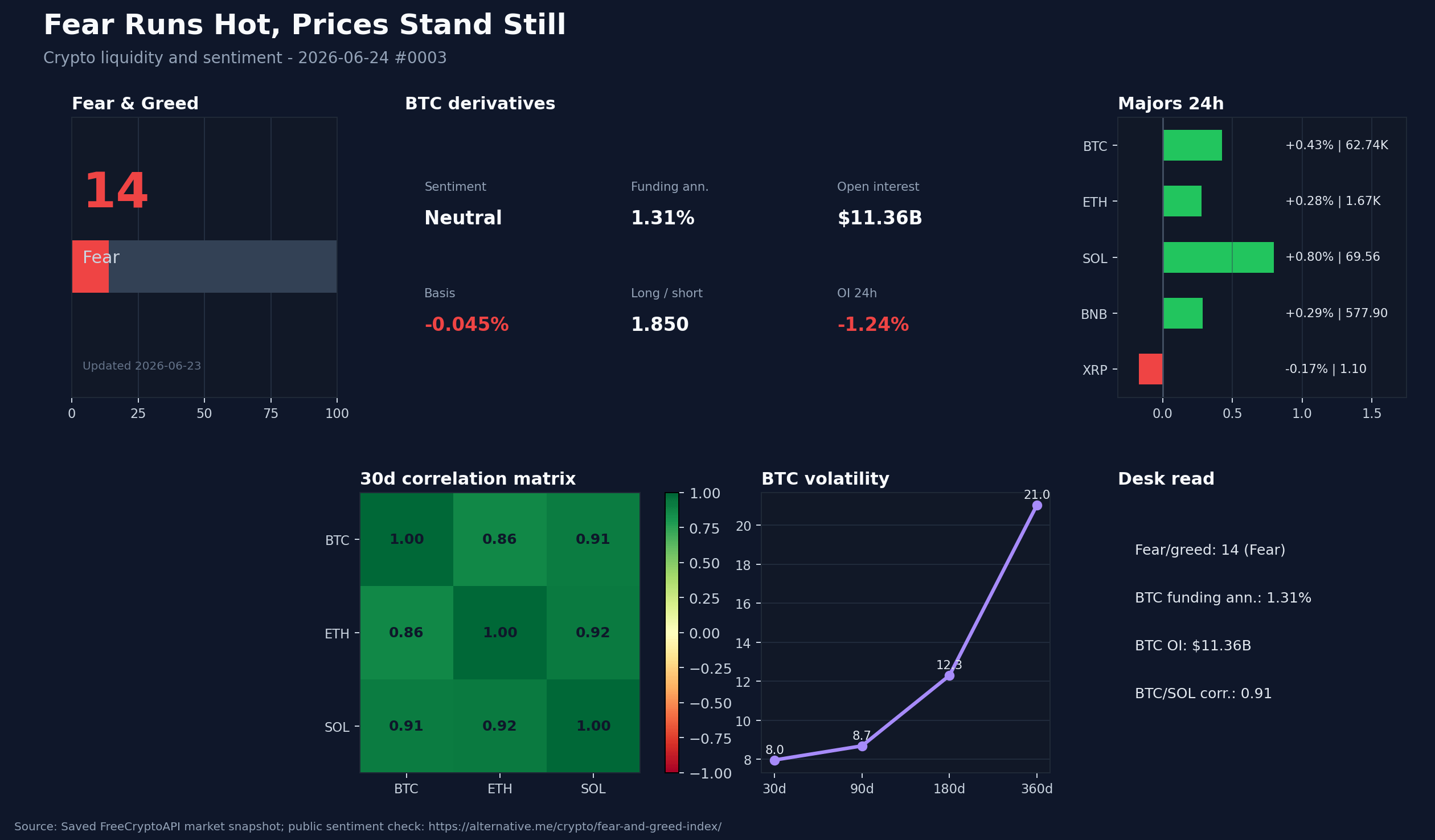

Crypto traded like a bruised but not broken liquidity proxy. The overnight market snapshot had BTC at 62,739.51 and ETH at 1,665.76, both nearly flat on the session even as crypto ETF proxies were weaker during U.S. hours.

Sentiment is still stressed. The public Alternative.me Fear and Greed Index sat at 17, or Extreme Fear, while the crypto derivatives snapshot showed BTC funding still mildly positive on average, long-short ratios above 1, and aggregate open interest around $11.36 billion with a small 24-hour decline. That combination reads as cautious but not capitulatory. Source: https://alternative.me/crypto/fear-and-greed-index/

DeFi remains large, but concentrated. The DeFiLlama snapshot showed roughly $473.6 billion in global TVL, $313.6 billion in stablecoin supply, and about $6.13 billion in 24-hour DEX volume. Ethereum still dominates the TVL stack, with BSC, Solana, Tron, Base, and Bitcoin making up the next tier, while Tron remains central in stablecoin circulation. Sources: https://defillama.com/chains; https://defillama.com/stablecoins

Real-Time Inflation Stays Tame

Truflation should be read here as a real-time signal set, not as a direct substitute for official BLS CPI or BEA PCE releases. The dates below are latest observation dates for each stream, not the collection date. For official CPI, PCE, labor, claims, JOLTS, or mortgage context, the article should use official or reliable public sources in the relevant macro sections rather than presenting monthly or weekly TRUF mirrors as live Truflation signals. Sources: https://truflation.com/marketplace/truflation-us-aggregated?modalOpen=true&modalWindow=signup

Live Truflation Signals

Divergence by Region

The United States still looks like the center of gravity. Strong June PMIs and a PCE-heavy calendar are keeping the front-end policy debate alive even as equities wobble. Source: https://www.fxempire.com/forecasts/article/u-s-dollar-tests-new-highs-as-composite-pmi-beats-estimates-analysis-for-eur-usd-gbp-usd-usd-cad-usd-jpy-1606109

Europe is the opposite mix: softer data tone, a weaker euro, and renewed worry that inflation could remain sticky enough to limit ECB flexibility.

Japan remains a currency story first. Yen weakness, auction softness, and live intervention risk are now part of the global liquidity conversation, not just a domestic issue.

China’s immediate significance is twofold: the upcoming PMI read and the new friction over critical-mineral shipments to Japan. That combination ties growth and geopolitics together in a way the rest of Asia cannot ignore.

India still reads as expansionary but cooling at the margin after June PMI misses versus estimates, while Turkey is pulling capital on the back of high carry and a calmer geopolitical frame.

Dollar, Yen, and Tech Angst

Reuters said the yen is still hovering near a forty-year low despite BOJ adjustments. For a macro desk, that keeps intervention risk live and makes USD/JPY one of the cleanest global liquidity telltales. Engagement was modest, but the account and topic carry high credibility.

Bloomberg’s markets account said the euro fell to its lowest level since August after weak data and dovish ECB commentary. That matters because a softer euro can tighten imported inflation politics for Europe even as growth softens.

Bloomberg also highlighted weaker demand at Japan’s five-year auction. That tweet matters less for the auction itself than for what it says about the fragility of the BOJ-yen-policy mix.

Another Bloomberg post said foreign investors are returning to Turkey for carry, market resilience, and reduced geopolitical risk. For macro desks, that is a reminder that high-real-rate EM pockets can still attract capital even while developed-market growth leadership wobbles.

Bloomberg’s report on China’s slowdown in critical-mineral shipments to Japan is the night’s most important geopolitical-growth crossover. It matters because supply frictions can hit industrial chains, sentiment, and Asia FX simultaneously.

Desk take: AI-led equity weakness, a firm dollar, and live Asia supply and FX stress are doing the tightening ahead of PCE, which raises the odds that the next data print matters more than the last headline.

The Next Stress Tests

Watch whether Core PCE on Thursday, June 25, 2026 comes in hot enough to validate the stronger dollar and pressure the front end.

Watch whether Germany’s Ifo and Australia’s inflation and labor sequence reinforce a global divergence story rather than a synchronized slowdown.

Watch USD/JPY for any sign that verbal or actual intervention risk is becoming binding.

Watch whether equity weakness spills into credit. If HYG and LQD stay orderly, this remains a leadership reset rather than a full risk event.

Watch China PMIs and the Japan minerals story together. That pairing can move copper, Asia FX, and industrial cyclicals at the same time.

Sources

Overnight market, rates, crypto, DeFi, calendar, and Truflation data snapshots used for index levels, curve points, release estimates, and nowcast tables.

https://www.wsj.com/finance/stocks/stocks-retreat-as-fears-deepen-about-strength-of-ai-boom-b0c9a310

https://www.barrons.com/articles/stocks-today-ai-jitters-chip-selloff-3b969fc0